Tax Implications of Capital Gains on Foreign Employee Stock Ownership Plans in India

Taxation of Capital Gains from Selling Foreign ESOPs in India

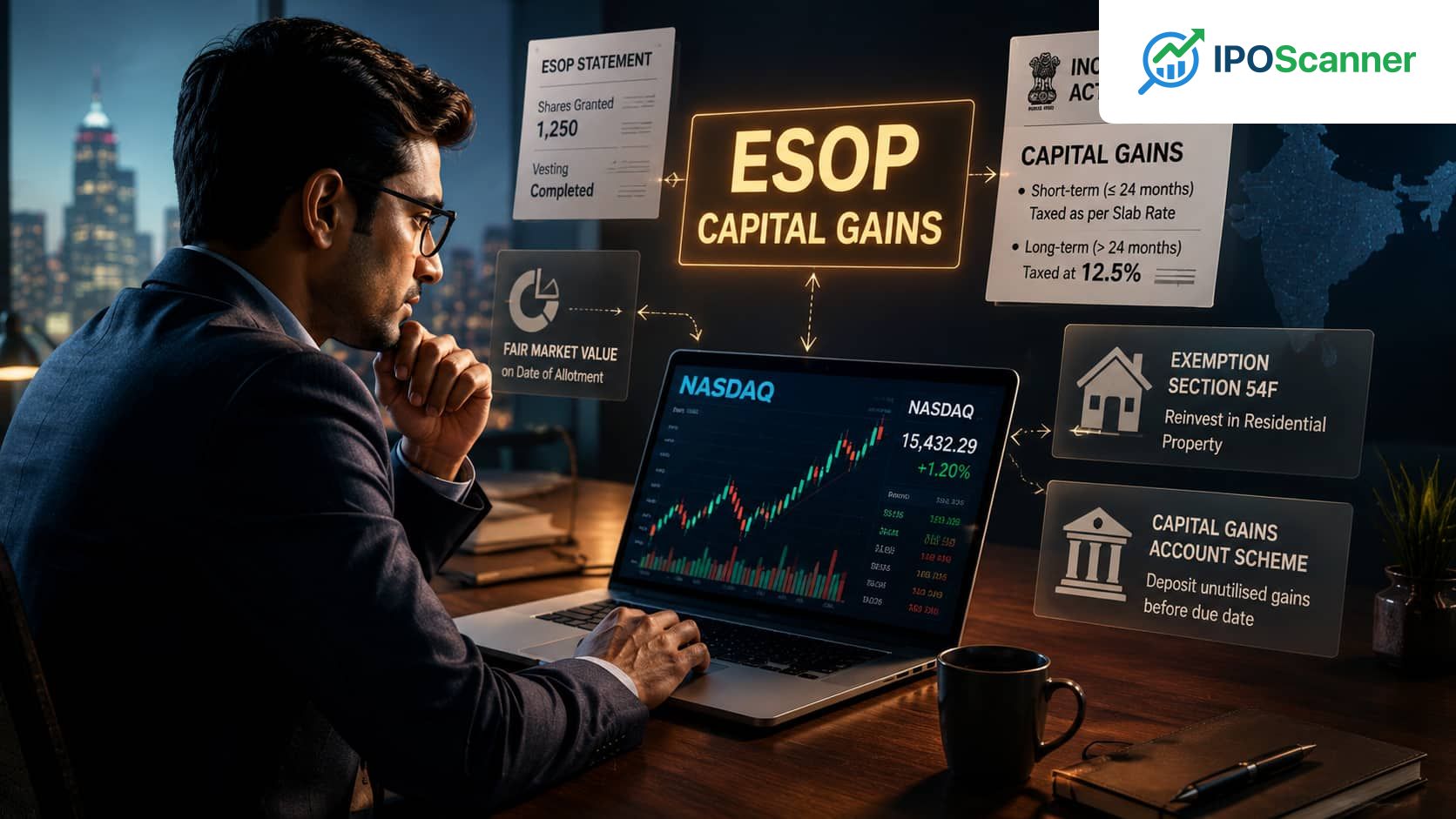

The Indian subsidiary of a US-based company listed on NASDAQ granted ESOPs to its employees, including Indian residents. When these employees sell the shares allotted to them, they may be wondering how the gains from the sale will be taxed in India. In this article, we will explain the taxation of capital gains from selling foreign ESOPs in India.

Taxation of Capital Gains

Shares allotted to employees by the parent company of their employer are considered capital assets. Profits made on the sale of any capital asset are taxed as capital gains. Therefore, profits arising on the sale of shares allotted to employees under the ESOP or any similar scheme are taxed as capital gains, like any other capital asset.

Holding Period and Capital Gains

Since the shares are not listed on any stock exchange in India, the profits from their sale will be taxed as short-term if they have been held for not more than 24 months on the date of sale from the date of allotment of such shares. If the shares have been held for more than 24 months, the profits are treated as long-term capital gains.

| Holding Period | Capital Gains |

|---|---|

| Less than 24 months | Short-term capital gains |

| More than 24 months | Long-term capital gains |

Tax Rates for Short-term and Long-term Capital Gains

Read also: Missing a Single EMI Payment Can Adversely Impact Credit Profile

The short-term capital gains are treated like normal income and added to the income, taxed at the slab rate applicable to the taxpayer. Long-term capital gains on the sale of such equity shares are taxed at a flat rate of 12.50 percent.

Indexation Benefits

The benefit of indexation is available to resident taxpayers only in respect of the sale of land and buildings acquired before July 23, 2024, and not in respect of all transactions of transfer of capital assets.

Exemption under Section 54F

Taxpayers can avail the exemption from long-term capital gains under Section 54F by investing the whole or part of the sale consideration received on the sale of shares for the acquisition of a residential house within the prescribed time period. To the extent such sums are not utilized for purchase or construction before the due date of filing of the income tax return, i.e. July 31, 2026, the amount must be deposited in a capital gains account with a bank on or before the due date of filing of the income tax return. The amount so deposited in a bank under the Capital Gains Account Scheme needs to be utilized for the purpose of purchasing or constructing the residential house within the prescribed time period from the date of sale of such shares.

More in General

Correcting Credit Score Errors: A Guide to Ensuring Accurate CIBIL Reports and Optimal Loan Eligibility

Missing a Single EMI Payment Can Adversely Impact Credit Profile

EPF Withdrawal Comes with Tax Implications: A Guide to Understanding the Consequences