Retirement Savings Options: A Comparative Analysis of EPF, NPS, and PPF

Retirement Planning for Investors: EPF, PPF, and NPS

Overview

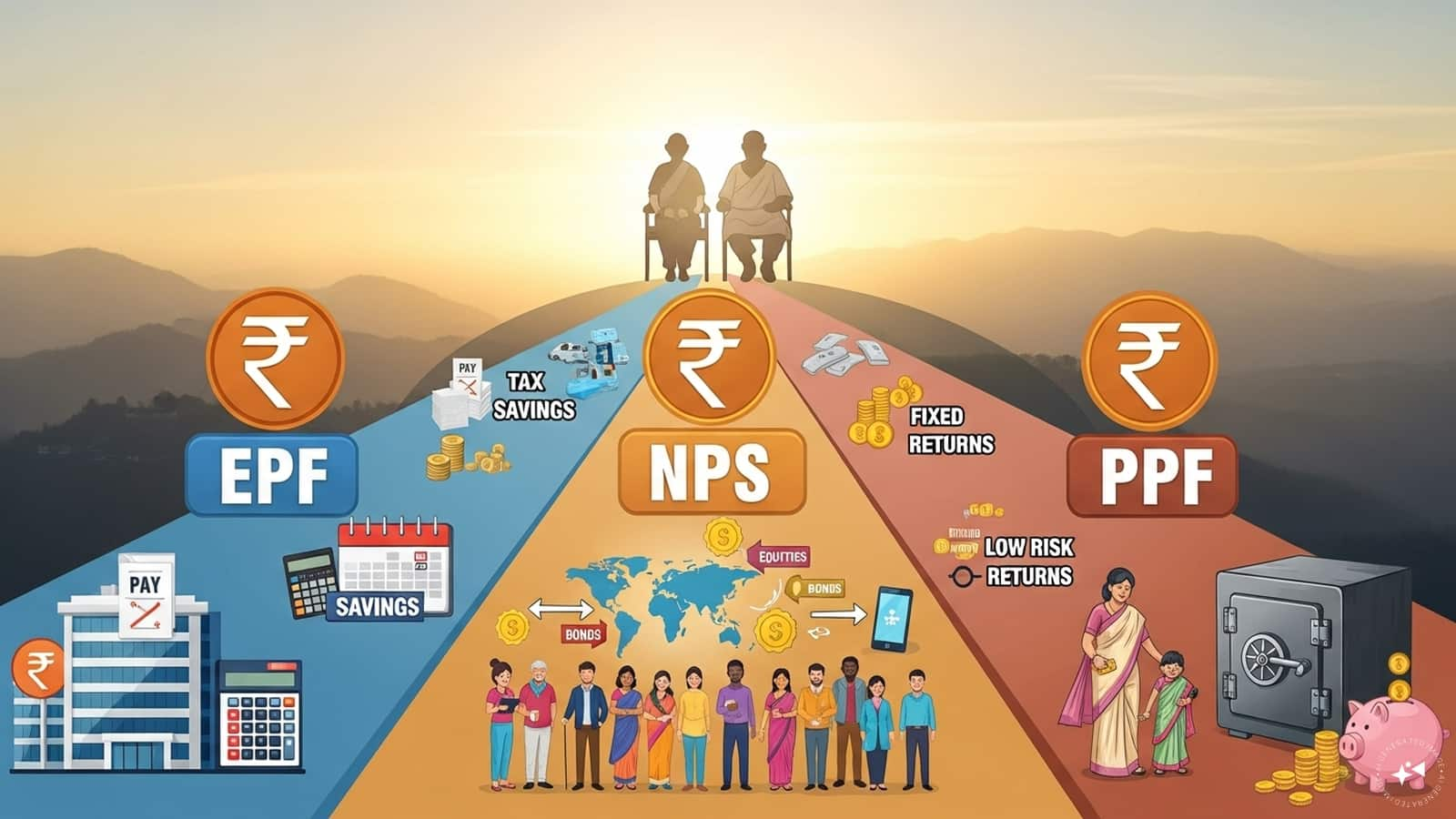

Investors often face difficulties in deciding between the Employees' Provident Fund (EPF), Public Provident Fund (PPF), and National Pension System (NPS) for retirement planning. Each scheme serves a unique purpose in building a retirement corpus, and the choice depends on an individual's life stage, risk appetite, and tax objectives.

EPF

The EPF is designed for salaried professionals in the organized sector with EPF benefits. It allows for low-risk, stable, and automatic retirement corpus creation through monthly salary deductions. This option is ideal for risk-averse individuals who want predictable retirement savings.

Key Features

- Tax-free maturity within prescribed limits

- Mandatory employer contribution, which remains tax exempt

- Low-risk, stable returns

Best Suited For

Read also: Missing a Single EMI Payment Can Adversely Impact Credit Profile

Risk-averse salaried individuals seeking predictable retirement savings.

PPF

The PPF offers safe, tax-free, long-term savings with a sovereign guarantee. It is suitable for conservative investors and self-employed individuals, offering tax-free interest and maturity proceeds with a 15-year lock-in period.

Key Features

- Tax-free interest and maturity proceeds

- 15-year lock-in period

- Flexibility to invest small amounts each year

Best Suited For

Conservative investors and self-employed individuals seeking tax-free savings.

NPS

The NPS addresses the gap in retirement planning by offering market-linked exposure at a low cost, making it more suitable for long-term wealth creation.

Key Features

- Market-linked returns for potentially higher long-term growth

- Extra Rs 50,000 tax deduction beyond Section 80C

- Low-cost structure with equity exposure

Best Suited For

Investors seeking market-linked growth at a low cost structure with equity exposure and a long time horizon.

Retirement Planning

Retirement planning works best when it balances safety with growth. Start early, invest regularly, and review your portfolio from time to time.

Simple Rule of Thumb

A combination approach using EPF or PPF for stability and NPS for growth potential is the most effective retirement strategy.

Investor Takeaway

Investors should consider their life stage, risk appetite, and tax objectives when choosing between EPF, PPF, and NPS for retirement planning.

More in General

Correcting Credit Score Errors: A Guide to Ensuring Accurate CIBIL Reports and Optimal Loan Eligibility

Missing a Single EMI Payment Can Adversely Impact Credit Profile

EPF Withdrawal Comes with Tax Implications: A Guide to Understanding the Consequences