GeneralMar 23, 2026

Claiming Section 54F Tax Exemption for Under-Construction Properties: A Guide to Key Timelines and Eligibility

Financial Report: Long Term Capital Gains Exemption for Under-Construction Flat

Key Points:

- Section 54F exemption allows individuals to claim relief from long-term capital gains tax on sale of equity shares, mutual funds, and gold bonds.

- Eligibility Criteria:

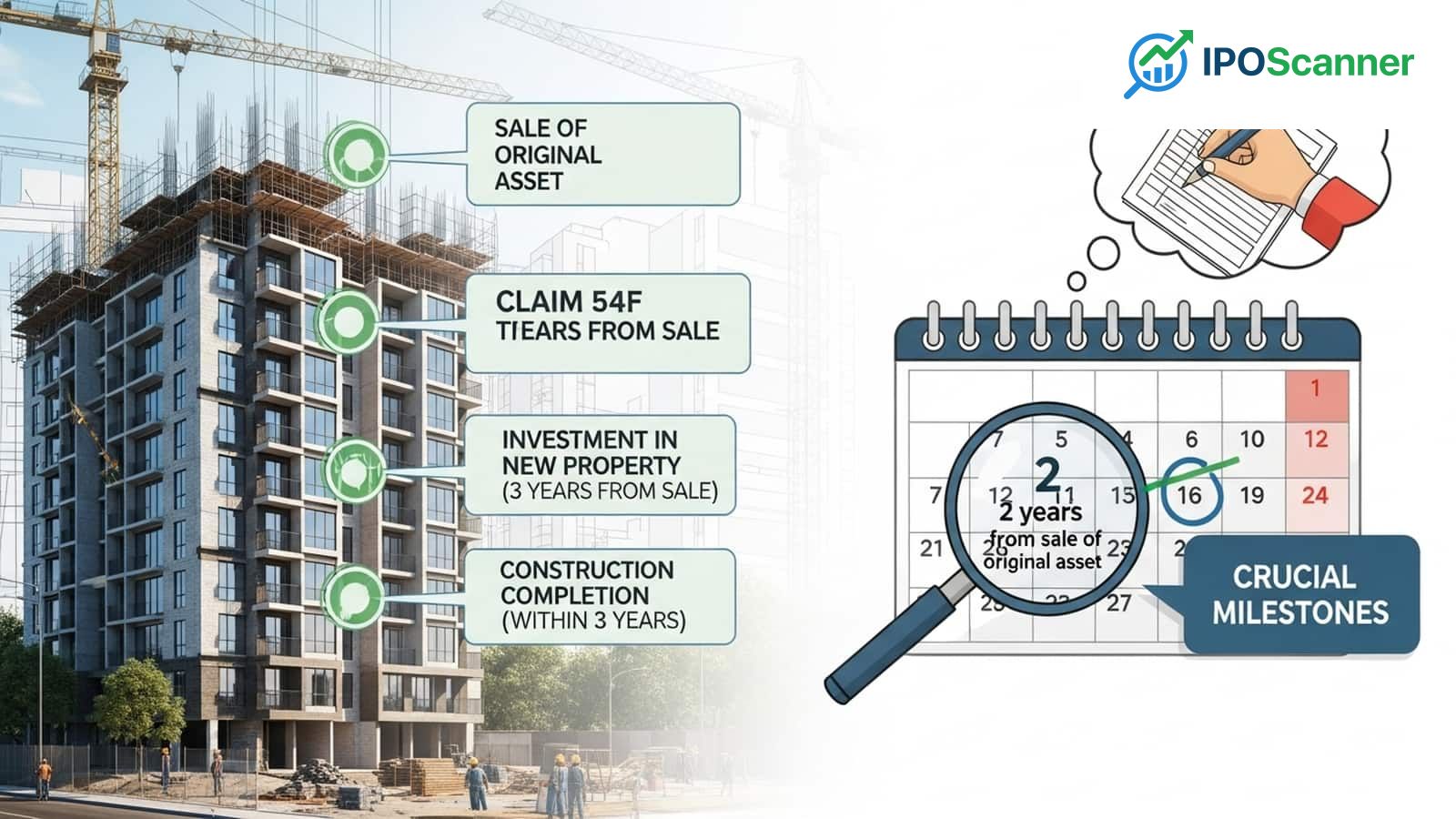

- Purchase/construction of a residential house property must be completed within three years from the date of sale of the capital asset.

- If the house is ready to move in, purchase must be done within two years from the date of sale.

- If the house is booked before sale, construction completion within three years from the date of sale is sufficient.

- Payment Timeline: Staggered payments made to the builder for an under-construction flat can still help claim long-term capital gains tax relief.

- Registration Timing: Date of registration of the agreement is not relevant for exemption purposes.

- Joint Registration: Adding a spouse's name to the agreement will not affect the ability to claim exemption, as long as the payment of the requisite amount is made by the individual.

Scenario Analysis:

- An individual booked an under-construction flat in May 2025 and made periodic payments to the builder, which will continue till May 2026.

- Major portions of these payments were made from the sale of long-term equity/MF/gold bonds.

- The individual can claim exemption under Section 54F for financial year 2025-26 based on the agreement and stage payments made to the builder, as long as the construction is completed within three years from the date of sale of the capital asset.

Conclusion:

- The individual can claim exemption under Section 54F for the long-term capital gains arising from the sale of equity shares, mutual funds, and gold bonds, as long as the construction of the under-construction flat is completed within three years from the date of sale.

- The date of registration of the agreement and the addition of the spouse's name to the agreement will not affect the ability to claim exemption.

Investor Takeaway

Investors should consider the eligibility criteria and timelines for claiming long-term capital gains tax relief under Section 54F.

More in General

General·4h ago

Correcting Credit Score Errors: A Guide to Ensuring Accurate CIBIL Reports and Optimal Loan Eligibility

General·10h ago

Missing a Single EMI Payment Can Adversely Impact Credit Profile

General·10h ago

EPF Withdrawal Comes with Tax Implications: A Guide to Understanding the Consequences

General·10h ago